A vibrant, prosperous economy isn’t a static entity. It undergoes a cycle of growth, maturity, and possibly decline, driven by a complex interplay of economic, political, and social dynamics.

Continue readingA vibrant, prosperous economy isn’t a static entity. It undergoes a cycle of growth, maturity, and possibly decline, driven by a complex interplay of economic, political, and social dynamics.

Continue reading

This article delves into the importance of forex reserves, the shifting trends in reserve currency preferences, and the emergence of de-dollarization, as nations seek to diversify their holdings and reduce reliance on the US dollar.

Continue reading

The UK had faced a continued slump in growth since the 2008 Global Financial Crisis, and the period of controlled inflation and lower costs of borrowing ended at the start of 2022. This incited the set of policies as well as the ideas and drivers underpinning them, which were then dubbed “trussonomics.”

Continue reading

In layman’s language, this article discusses the too-big-to-fail phenomenon, the subprime crisis of 2008, Lehman Brothers bankruptcy, AIG’s bailout, Credit Default Swaps, and the current Credit Suisse situation.

Continue reading

Companies from all sectors and even those who aggressively hired employees during the pandemic are on the verge of hiring freezes due to macroeconomic uncertainty hovering around the world. Companies like Amazon, Shopify, and Peloton were some big names that almost doubled their workforces to manage smoothly through the pandemic surge and meet customer demand.

Continue reading

Behavioral finance combines psychology with finance to examine investor behavior and understand how people make financial or investment decisions, individually and collectively. The groundbreaking work of psychologists Daniel Kahneman and Amos Tversky in the 1970s-1980s revealed striking insights into the complex ways in which the human mind operates.

Continue reading

UPI has become the world’s largest real-time payments system. In FY2021-22, it accounted for nearly 40% of the 55 billion transactions that took place in India during the year. Total transactions crossed ~ Rs. 84 lac crore (breaching the $1 trillion mark) in the same year.

Continue reading

The annual inflation rate in the US unexpectedly accelerated to 8.6% in May 2022, the highest since December of 1981. As a result, the Fed raised its benchmark rate by 75 bps — the biggest increase since 1994.

Continue reading

SPACs or Special Purpose Acquisition Companies have garnered a lot of boardroom attention post the successful IPO listing of companies like Virgin Galactic, WeWork, and ReNew Power. SPACs’ popularity was limited only to the U.S. until now, but now they have begun being considered by regulators worldwide.

Continue reading

Stablecoins are cryptocurrencies that are designed to provide users with the benefits of cryptocurrencies without the high volatility of conventional cryptocurrencies such as bitcoin or Ethereum. While conventional cryptocurrencies allow users to carry out transactions, their highly volatile nature makes them economically unviable for such transactions. This is where stablecoins come in.

As the name suggests, these cryptocurrencies are relatively stable in their value. Stablecoins are generally pegged to another fiat currency or a commodity. In order to achieve higher stability, these currencies need to be collateralized. This provides users with an assurance that the stablecoin or token won’t lose its value. They are backed by a reserve of other fiat currencies such as the US dollar, commodities, or even other cryptocurrencies.

While most stablecoins are collateralized by other fiat currencies or commodities, we have seen the emergence of a new kind of stablecoin, called algorithmic stablecoins. These coins differ in the way their peg to another currency is maintained. Instead of being backed by collaterals in fiat currencies, these stablecoins are managed by an algorithm that automatically tries to keep the balance. Let’s understand this with the example of the Terra blockchain, which includes TerraUSD (UST) – a stablecoin, and LUNA – a cryptocurrency that backs UST.

UST aims to maintain a peg ratio of 1:1 with the US dollar, which means that each UST token should be worth $1. The Terra ecosystem consists of UST and LUNA, where UST is the stablecoin while the system uses LUNA to absorb volatility. The system allows users to exchange UST and LUNA. Users can ‘burn’ $1 worth of LUNA to mint 1 UST token, which is equal to $1, or they can burn 1 UST token to get $1 worth of LUNA. This system is an ‘on-chain’ system, which means that users can exchange $1 worth of LUNA for 1 UST token irrespective of its price in the off-chain market or other exchanges. The market price of UST may change due to changes in the demand and supply of the token. Decentralized apps on the Terra blockchain use UST for transactions, and this dictates the overall demand for UST. The higher the number of apps on the blockchain, the higher the demand for UST and LUNA.

Let’s consider a situation where the price of UST in the market reaches $1.05. Here, users can burn $1 worth of LUNA for 1 UST on the Terra system and sell the same at its market price, i.e., $1.05 in other exchanges. A user can make $0.05 of profit with minimal risk. Similarly, if the value of UST goes below $1, let’s say $0.95 in the markets, users can buy UST from the open market and burn it on the Terra system to get $1 worth of LUNA, earning them a profit of $0.05. To put it simply, if UST falls below the $1 peg, the system mints LUNA and burns UST to try and bring it back to the $1 peg while the value of LUNA decreases as more of it is minted. The system allows users to do this process continuously until the price of UST reaches $1. This mechanism is carried out using an algorithm, and it allows UST’s value to be relatively stable at around $1 while LUNA absorbs volatility. While this system appears to be straightforward, there were a few problems that led to the eventual crash of LUNA and UST.

One of the major problems with such an algorithm is that it can only maintain the stablecoin’s peg for small and temporary fluctuations in prices. UST essentially functions as a digital US dollar, but ultimately it is a cryptocurrency and not the US dollar itself, which increases the risk for investors. Market conditions and factors such as the peg slipping below $1 can cause the value of UST to fall significantly in the open market. This creates increased selling pressure on UST as investors will look to withdraw and invest in other alternatives. As discussed earlier, in order to bring UST back up to $1, the system mints LUNA. If the dip is small, there wouldn’t be any problems. However, if the selling pressure is too high, UST will keep falling, and the system will keep on minting more and more LUNA to try and get the value of UST up. This increased supply of LUNA leads to a decline in the price of LUNA as well. This situation is a kind of a death spiral, and eventually, the system fails to bring the price of the stablecoin back to its peg.

Another issue was with the lending and borrowing mechanism on Terra. The terra ecosystem had a protocol known as the Anchor protocol. This allowed people to lend and borrow UST and LUNA. Depositors who deposit their cryptocurrency earn interest, while borrowers pay interest. However, one important thing that must be noted is that instead of these interest rates being determined by demand and supply, Terraform Labs, the company behind the Terra ecosystem, had fixed this interest rate at a whopping 20% on UST. This was one of the highest in all of crypto. This attracted a lot of demand for UST, and a majority of the holdings in UST were in the form of these deposits earning a 20% rate of interest. The major risk here is that such high interest rates are not sustainable. The borrowers on Terra paid considerably less interest on their borrowings as compared to the interest paid to depositors. This meant that the company had to subsidize this by paying depositors out of the company’s reserves because the revenue from borrowers was just not enough to cover the payments to depositors.

The Terra ecosystem was conceived by Do Kwon, a South-Korean cryptocurrency developer. He had worked in Silicon Valley for a short period of time before he started building Terraform Labs. Several reports have stated that company insiders claimed Do Kwon to be an autocratic leader, and he would micro-manage and make all decisions himself. While the coin holders did have voting rights on decisions, ultimately, the decisions were influenced by Do Kwon. The system that was supposed to be decentralized showed signs of being completely centralized. Decisions such as keeping the interest rate fixed at 20% and not keeping any restrictions on people withdrawing their deposits were influenced by him. These relaxed policies were put in place to create more demand for UST artificially. Many top executives had also resigned from their positions with legal disputes. In addition, just days before LUNA and UST crashed, Do Kwon had filed to dissolve Terraform Labs in South Korea, which was a major warning sign.

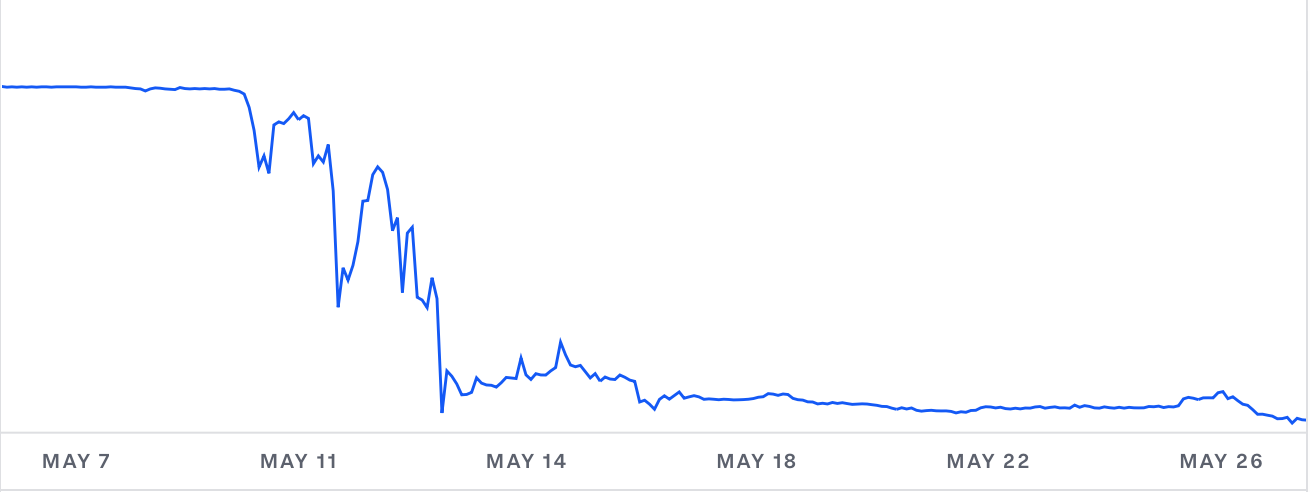

The Terra ecosystem had grown rapidly due to the high interest rates. It was being used on hundreds of decentralized applications for managing transactions. Due to strong demand, LUNA had reached an all-time high of around $119, and the entire system was valued at $45 billion. However, UST’s peg started slipping in May 2022, i.e., it fell below $1, creating a panic among investors. This was followed by huge withdrawals from the deposits that were earning interest on the Anchor protocol. Around $4 billion worth of UST was dumped, causing immense selling pressure. Investors resorted to panic selling, and the value of UST kept falling. As discussed earlier, this led to a death spiral. To maintain UST’s peg, the system minted more and more LUNA while investors were losing confidence and selling their tokens. This led to a huge crash in LUNA and also resulted in UST losing its peg. The following chart shows the decline in the value of LUNA and UST.

Within a matter of days, the entire $45 billion market capitalization was wiped off. The Luna Foundation Guard (LFG) was set up as a foundation to back the Terra ecosystem. It had reserves of over $450 million in US dollars and $1 billion worth of bitcoin. These reserves were meant to be used in situations where UST loses its peg. However, during the crash, the selling pressure was so high that these were not effective. In addition, investors feared that LFG would liquidate its massive bitcoin reserves, which led to a cascading effect where bitcoin’s price fell too, ultimately reducing the effectiveness of LFG’s reserves.

LUNA had become one of the five largest cryptocurrencies at its peak, and the Terra ecosystem was being used by many decentralized applications. A crash in such a mainstream cryptocurrency sent ripples across the crypto world. U.S. lawmakers demanded increased regulation of stablecoins, especially algorithmic stablecoins, to protect investors. Some experts expressed their opinions that the crash was due to a series of coordinated activities, i.e., the massive withdrawals from the system were carried out by a few large institutions such as hedge funds who knew the system’s vulnerabilities and had created short positions in Terra. All the problems discussed above had been raised by multiple experts before the crash. However, a large number of investors had blind faith in the system and ignored all red flags. Many investors lost their life’s savings in the crash.

After the fiasco, Do Kwon announced a revival plan for the Terra ecosystem with the introduction of LUNA 2.0. This entailed forming a new blockchain without the UST stablecoin, while the old system was to be renamed Terra Classic. The new chain kept the name Terra. Under this plan, the number of new LUNA tokens was reset and fixed at 1,000,000,000. Investors’ older holdings were converted to Terra Classic.

Additionally, at the launch of the new token, free tokens were proposed to be distributed to the Terra community, people who are either Terra Classic stakeholders, holders of residual UST, or core developers of Terra Classic. This process of distributing free tokens is known as an ‘airdrop.’ According to this plan, Terra would become a community-owned blockchain that is completely decentralized. This revival plan was approved by a vote of community members, with 65% voting in favor of this plan. The new blockchain went live on exchanges on 28 May 2022. Due to a lack of confidence and increased skepticism, it experienced increased volatility and could not sustain its price. It was listed at $18.75, but it is currently trading at nearly one-third of its listing price.

This article is authored by Preet Singhvi