Introduction

SPACs or Special Purpose Acquisition Companies have garnered a lot of boardroom attention post the successful IPO listing of companies like Virgin Galactic, WeWork, and ReNew Power. SPACs’ popularity was limited only to the U.S. until now, but now they have begun being considered by regulators worldwide.

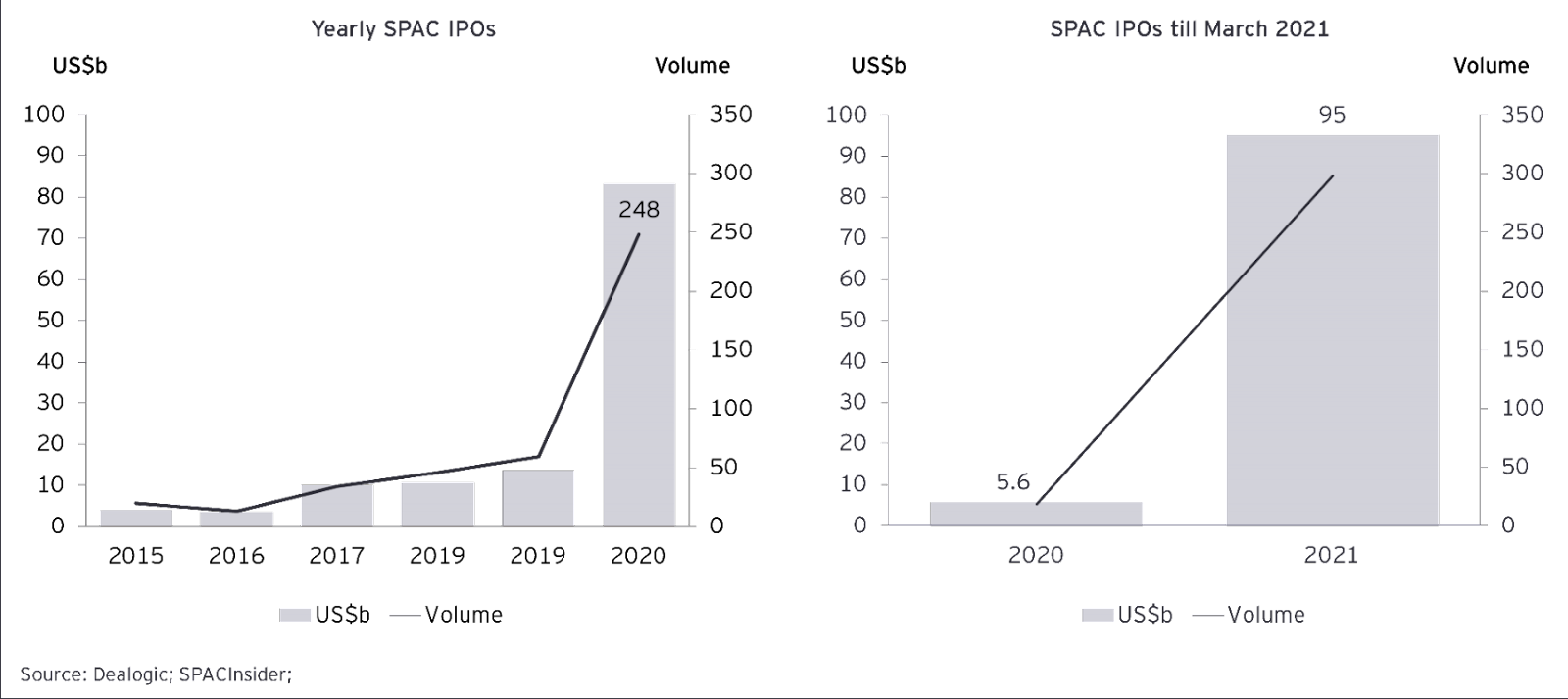

2020 was a record-breaking year for IPOs via SPACs in the United States, where 247 companies were incorporated with $80 billion in investment and accounted for more than 50% of new publicly listed U.S. companies. While in the first quarter of 2021 alone, 295 companies were formed with $96 billion in investments that have created a new milestone concerning sheer volume and gross proceeds.

History of SPACs

SPACs didn’t have a great start when they first appeared in the 1980s as blank-check corporations. They were not regulated well back then and, as a result, were plagued by Penny-stock fraud, costing investors more than $2 billion a year. Therefore, the government stepped in to provide much-needed regulation and standardize the launch of IPOs via SPACs. These blank-check corporations were rebranded as SPACs under a new regulatory framework and have been around in the U.S. for more than 20 years now.

Although, it has grown in popularity recently for multiple reasons that benefit businesses, promoters, and investors. These include the credibility of sponsors, the growth potential of target businesses, the lengthy-time & process involved in traditional IPOs, and the availability of dry powder in the post-COVID-19 era. Additionally, substantial funds have been raised by SPACs in the recent past across the globe, and one could anticipate seeing many SPAC transactions being consummated in the near term.

| Issuer | Total Proceeds (US$ million) |

| Pershing Sq Tontine Holding Ltd. | 4,000 |

| Churchill Capital Corp IV | 2,070 |

| Soaring Eagle Acquisition Corp | 1,725 |

| Foley Trasimene Acquisition Corp II | 1,467 |

| Churchill Capital VII | 1,380 |

| KKR Acquisition Holdings I | 1,380 |

| Austerlitz Acquisition Corp II | 1,380 |

| Social Capital Hedosophia VI | 1,150 |

| Jaws Mustang Acquisition Corp | 1,035 |

| Foley Trasimene Acquisition | 1,035 |

A Typical SPAC’s Lifecycle

SPACs are typically launched by experienced management teams with a proven track record and a thorough understanding of the industry or market sector. The sponsors of a SPAC are its founders, and as investors entrust funds to their professional judgment/expertise, they become the public face of a SPAC.

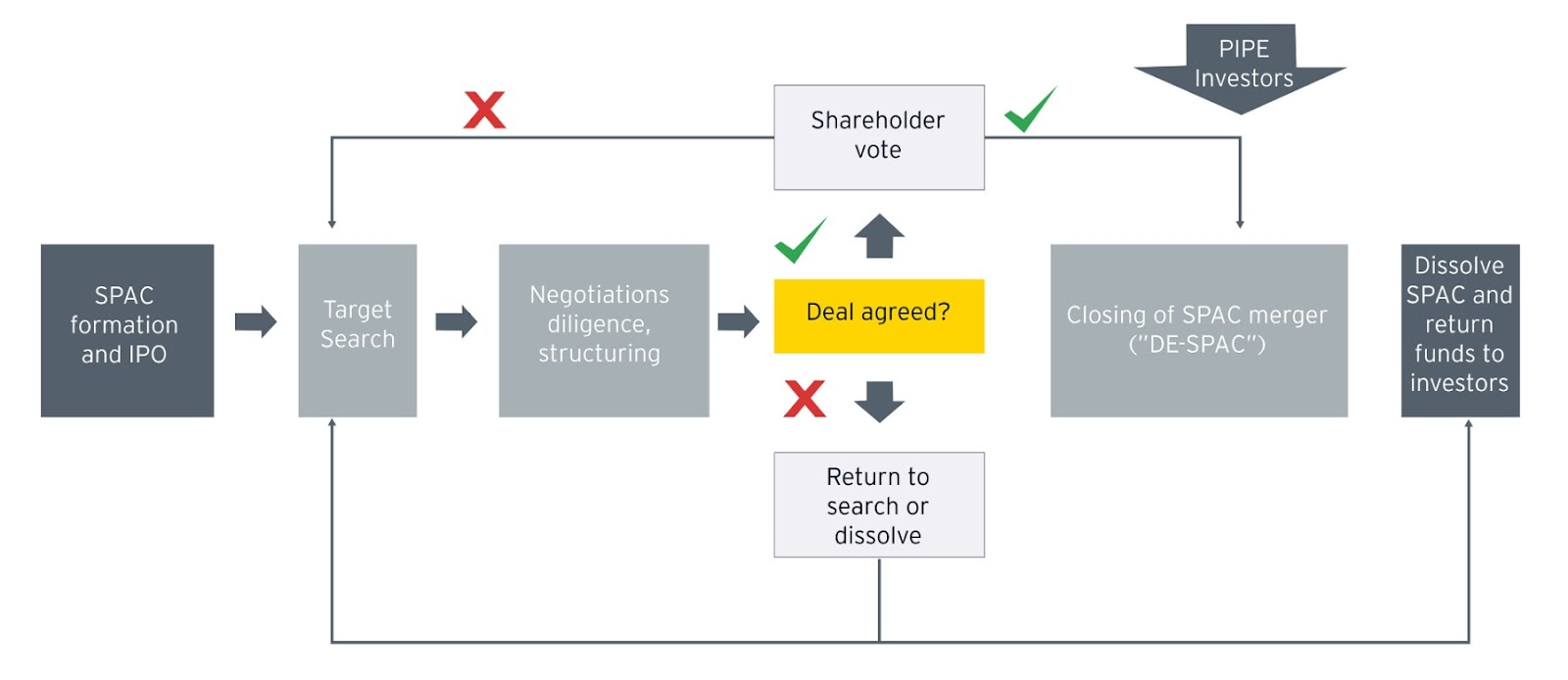

A SPAC’s sponsor/management team registers the SPAC shares with the Securities and Exchange Commission (SEC), holds a pre-IPO roadshow, and raises capital via a SPAC IPO. It is conducted in exchange for the issuance of SPAC shares listed on a stock exchange, typically at US$10 per share. The SPAC’s IPO proceeds are held in a trust until the business merger is finalized.

Once a target has been identified, the SPAC purchases it (for example, through a consolidation/merger) in what is known as a “de-SPAC” deal. SPACs could consider raising funds from PIPE investors, provided additional funds are needed at this stage (for the target acquisition).

The target company becomes a subsidiary of the SPAC or a new holding company whose shares are listed on the stock exchange after a successful de-SPAC transaction. Assuming a SPAC cannot conduct a de-SPAC transaction within the time limit, the money raised in the initial SPAC IPO is returned to investors in this situation, and the SPAC dissolves.

The ‘Distinguishing Factor’

Since the SPAC investors have no idea which private firm the SPAC aims to merge with, their investment decision is based on their faith in the investor or entity attempting to make the acquisition. Shaquille O’Neal and former Speaker of the House Paul Ryan were two of the most well-known people to launch SPACs in 2020.

Furthermore, SPACs are frequently supported by well-known investment banks, such as Goldman Sachs or JPMorgan, enhancing their trust among investors. In 2020, the average initial return after SPAC IPOs was higher than in previous years. Traditional IPOs, on the other hand, generated better equity returns in 2020 than SPACs.

The profit potential for sponsors, suitable risk-adjusted returns for investors, and a reasonably appealing procedure for raising funds for targets are all created by successful SPACs. The more value that can be created, the more likely a SPAC will be able to strike an agreement that is suitable to all parties and result in a successful merger.

But why choose SPACs for IPO listing?

Benefits To The Stakeholders

There are three main parties involved, namely sponsors, investors, and targets, that have a unique set of concerns and benefit from the SPAC transaction differently.

- Sponsors: The SPAC process is generally initiated by sponsors who purchase equity in the SPAC at more favorable terms than investors in the IPO. They invest non-refundable risk capital in covering operating expenses; therefore, the sponsor generally holds around a 20% stake in the post-IPO SPAC deal. Once the sponsor identifies a promising target and convinces the target of a strategic business combination, this 20% holding will eventually be converted into a respective stake in the target’s business. It becomes a motivating factor for the sponsor to find an attractive target with immense potential value.

- Investors: Institutional investors and highly specialized hedge funds have made significant investments in SPAC. The original investors in a SPAC buy shares before identification of the target company, solely believing and having faith in the sponsor. They generally receive two classes of securities: common stock (typically priced at $10 per share) and warrants that allow them to buy shares in the future at a pre-specified price (usually $11.50 per share). These warrants are an additional incentive for investors to subscribe to the SPAC issue, which allows them to move forward with the deal or withdraw and receive their original investment back with interest.

- Targets: The main advantage for a target to choose a SPAC merger over the traditional IPO process is the faster execution and upfront price discovery. Additionally, the SPAC route provides the target company multiple benefits in the form of lower marketing costs and easy access to operational expertise. Compared to a traditional IPO process, where the regular underwriting fee is typically 7%, these costs are generally lower in the case of a SPAC deal.

Why Haven’t Emerging Countries Incorporated SPACs yet?

So far, the SPACs couldn’t gain much traction in the emerging countries. This is because of several legal and logistical challenges.

For instance, Indian regulations are far more stringent as the Companies Act of 2013 specifies that any company that does not begin business operations within a year after incorporation may be forced to shut down.

Furthermore, a firm must also have tangible assets of Rs. 3 crores three years before an IPO launch and a minimum average consolidated pre-tax operating profit of Rs. 15 crores in any three of the previous five years. It isn’t all; SEBI has a slew of other requirements for businesses to meet, making the procedure complicated and time-consuming.

However, a new proposal from the Ministry of Corporate Affairs (MCA) may change this soon.

Even yet, if investors decide to join a SPAC, they must first obtain permission from the National Company Law Tribunal (NCLT), which could take a long time. India is stringent with its regulations because SPACs are eerily similar to shell companies that are only established to evade tax bills or for illicit activities such as money laundering.

However, India has learned that SPACs are much more than that. As a result, the Securities and Exchange Board of India (SEBI) and the Ministry of Corporate Affairs are drafting draught legislation to govern this market properly.

Conclusion

The SPACs segment is a rapidly evolving story. Our financial markets are being transformed and reshaped by the remarkable emergence of the SPACs. Regardless of market conditions, recognizing the risks and rewards associated with a SPAC merger is critical to success. Hence, investors should stay informed and vigilant to seek potential benefits.

No comment yet, add your voice below!