Introduction

The annual inflation rate in the US unexpectedly accelerated to 8.6% in May 2022, the highest since December of 1981. The sudden rise in the prices of gasoline (48.7%), fuel oil (106.7%), and electricity (12%) had a spillover effect on energy prices as well, which rose by 34.6%, the highest since September of 2005. The peak inflation today is increasingly supply-driven rather than demand-driven, which limits the growth and restricts the central bank from loosening policy even in the event of subdued growth. The 40-year high inflation topping 8% annually in recent months is digging a hole in the pockets of people who are already paying more for gas, groceries, and everything else. The Fed has multiple tools to tackle this situation; however its ability to influence interest rates is the most prominent and effective monetary policy tool. As a result, the Fed raised its benchmark rate by 75 bps — the biggest increase since 1994.

Expressing Money Demand: Let’s Get Back to Theory

The money market is in equilibrium when the money supply (Ms) set by the central bank equals aggregate money demand (Md). Algebraically, we can write it as below:

Ms = Md

Ms = P x L(R,Y)

Ms/P = L(R,Y)

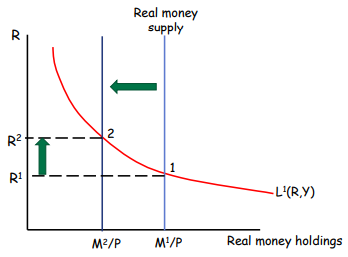

Given the price level (P) and the level of output (Y), the equilibrium interest rate (R) is the one at which aggregate real money demand equals the real money supply. Suppose the central bank wants to raise interest rates to dampen spending by firms and consumers; to reduce inflation, it induces a decrease in the money supply from M1/P to M2/P.

The below graph demonstrates the effect of the interest rate hikes by The Fed (R1 to R2), which reduces the money supply in the economy to tackle inflation. It increases borrowing costs, making loans more expensive for businesses and consumers, and everyone spends more on interest payments.

Performance of Stock Market During Previous Rate Hikes

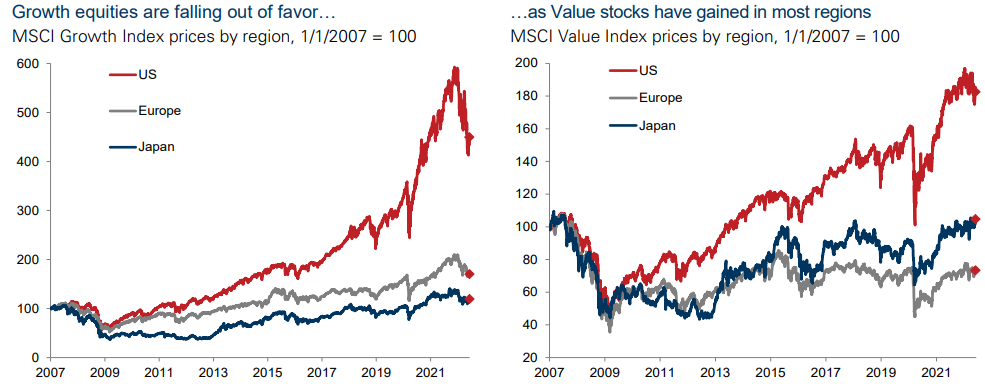

The hiked interest rate has implications that ripple throughout the entire economy, impacting every sector as mortgages, housing loans, car loans, and business loans become more expensive. As a result of higher borrowing and increased finance costs, the businesses tend to amend or pause plans for growth due to a temporary cash-flow crunch. Although the rate hike does not affect every sector equally, it especially hurts growth (e.g., SaaS, Tech, etc.) stocks as investors tend to look for stable opportunities during uncertain market conditions. The inflationary peak benefits cyclical equities, financial services, and consumer discretionary stocks.

The below-mentioned graph depicts, how the growth stocks globally saw a dip when value stocks outperformed the market.

The rate hike doesn’t impact every sector equally; banking & financial stocks benefit from increased interest rates as borrowing cost becomes expensive, leading to higher margins (cost of capital also increases but the rise in lending rates usually more than offsets the cost of capital). Thus, in markets like this, selective investors or so-called ‘stock pickers’ can have the upper hand who happens to identify the correct stocks/sectors for investment purposes.

How Did Broad Market Indicies Perform After Rate Hikes?

Contrary to the fact that the stock market tends to underperform during rate hikes, it has surprisingly given positive returns during the last five rate hike cycles. It is illustrated by the three leading U.S. stock market indices, which only declined during one cycle between June 1999 to January 2001. When factored together, the S&P 500 saw a median increase of 30% across all the rate hike cycles; Dow Jones Industrial Average delivered a return of 17.40%, while Nasdaq generated 26.90% in the same period.

Asset Allocation Strategy During Rate Hike

The Fed kept interest rates near zero during the COVID-19 pandemic to boost the consumption by making people spending more on goods & services. However, in 2022, the Fed’s monetary policymaking body would be raising its benchmark interest rates to curb the soaring sky-high prices and keep inflation under control. Asset allocators face a particularly daunting task in constructing portfolios to withstand the messy mix of possible macro outcomes due to rising inflation, central bank tightening, and slowing growth.

Based on the anticipation of the interest rate hike, several investors and fund houses have amended their investment strategy and made re-allocations to the portfolio. Diversifying the portfolio becomes crucial during different market cycles as inter-relationship between four primary markets — commodities, bond prices, stocks, and currencies work differently in different cycles. Thus when the interest rate rises, investors tend to reallocate assets in their portfolios.

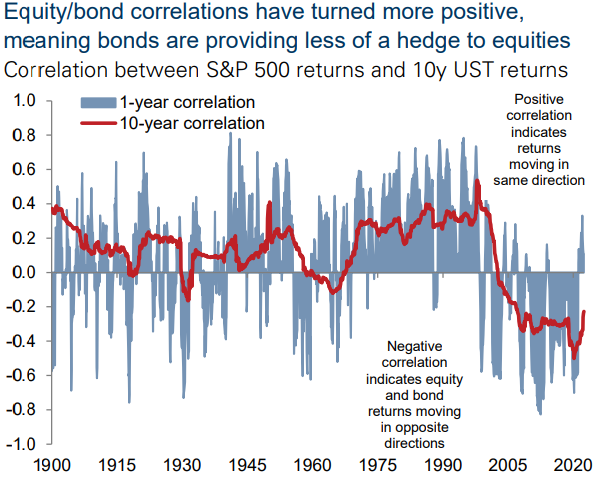

A well-diversified portfolio relies on bonds as a counterweight to riskier stocks. Stocks and bonds are generally negatively correlated to one another, and one rationale behind this relationship stems from the fact that bonds are usually considered less risky investments than stocks. Therefore, when the interest rate rises, the bond market is anticipated to see a surge in demand as investors move out of stocks and put money in bonds.

Portfolio risk depends on the variance of asset, the weight of each asset, and the correlations between the returns of the assets in the portfolio. However, lately, this has not been the case since equity and bond correlations have turned more positive, which results in risk averaging and does not provide any risk reduction. The chart below shows how the equity and bond correlation has turned more positive over the years. The gain from diversifying is closely related to the value of the correlation coefficient – the degree of risk reduction increases as the correlation between the rates of return on two securities decreases, and vice-versa.

Investors can also seek to look out for floating-rate funds that invest in bonds whose interest rate changes based on external benchmarks. Other alternatives like gold and equity-neutral market funds are good options for investors looking for low correlation to stocks and more diversification than bonds.

Implications of Rate Hike

The primary goal of the interest rate hike is to curb inflation and bring down the soaring high prices by slowing down economic activity to an extent. Due to higher interest rates, the borrowing cost will also increase, refraining consumers from making large purchases and pulling back their spending.

The implications of the same can be seen in the housing market, where the mortgage demand has significantly slowed down. The 30-year fixed mortgage rates have increased from 3.22% to 6.28% in just six months, refraining consumers from purchasing houses as the loans have become expensive. In a nutshell, as the load of increased interest cost is passed on to consumers and businesses, the borrowing declines, eventually leading to less consumption until the prices return to the equilibrium price level.

Conclusion

The Federal Funds Rate (FFR) is the rate set by the Federal Reserve Board that determines the interest rate at which financial institutions (such as banks) borrow and lend money to one another. The Fed closely watches inflation indicators such as Consumer Price Index (CPI) and Producer Price Index (PPI) to gauge inflation and takes appropriate actions to keep rising prices under control. Thus, any change in interest rate is watched closely as it has ripple effects across the entire economy, which usually takes a year to set in. The stock market is always forward-looking and thus, a response to the change in rate is often more immediate.

No comment yet, add your voice below!