Introduction

The world was just recuperating from the COVID-19 induced economic shocks in 2022, but two major growth risks are looming large against a backdrop of alarmingly high inflation. The world economy was already facing a multi-year high inflationary pressure which got more severe due to the Russia-Ukraine conflict, which further led to the tightening of the economic cycle by the Fed.

Further, the geopolitical tension between Russia and Ukraine has crippled the European economy due to its huge dependence on the Russian energy supply. This could lead to a stagflationary period of persistently higher inflation and low (or even negative) growth in the coming time. Historically, the U.S. yield curve is a reliable indicator of recession risk, which in recent times has seen a mild inversion that led to various economic projections suggesting that a Recession is coming!

The 1970s Economic Malady & Oil Embargo Crisis

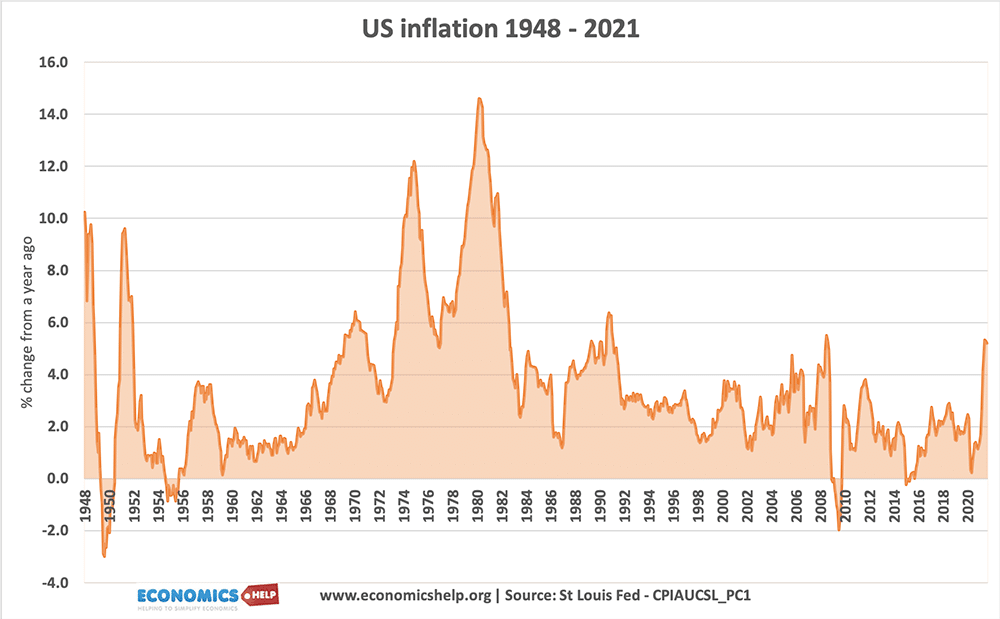

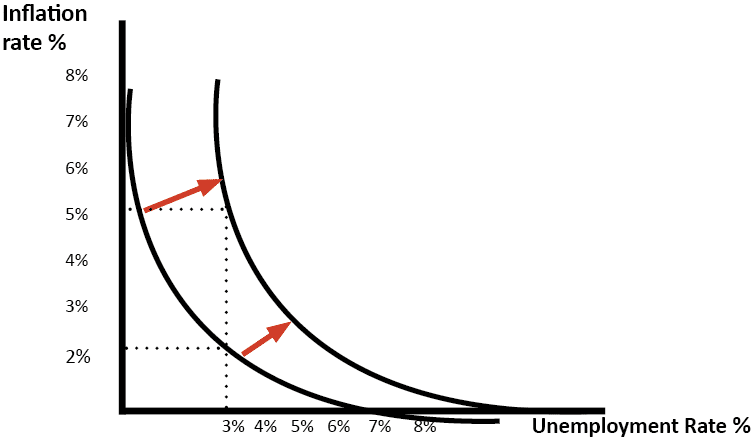

Stagflation is a perfect storm of economic ills in which the growth comes to a halt, inflation reaches the exosphere, and unemployment also remains steadily high. Periods of stagflation were prevalent in the 1970s and 1980s in most major economies due to the oil shipping embargo on the United States & Israel’s European allies. This caused oil prices to skyrocket by more than 300%, the inflation rate reached double-digits, unemployment soared to 10.8%, and the S&P 500 Index lost more than half its value. The prevalence of stagflation during this period challenged the dominant economic theory of the time, Keynesian Macroeconomic Theory, and was partly based on the Phillips Curve. It is an economic model that was used to argue that there was an inverse relationship between unemployment and inflation. Since then, economists have identified many potential factors that cause stagflation which primarily include sudden negative supply shock and harmful governmental policies.

The Keynesian Macroeconomic Theory suggests that there is a trade-off between inflation and unemployment. However, economist William Phillips suggested that during Stagflation, The Phillips Curve shifts to the right, giving a worse trade-off. Due to the western support of Israel during the Yom Kippur War, OPEC declared an oil shipping embargo which coincided with a move of manufacturing jobs outside the U.S. to save on labor costs. Additionally, the rising expense of the Vietnam war also led to a prolonged period of stagflation where elevated oil prices caused economic turmoil and sudden inflation.

Fast Forward To 2022…

Consumer demand has seen a sharp rebound in the last year, U.S. inflation is rising at its fastest pace in the last 40 years, and economic growth is expected to moderate from 2021’s red-hot levels. These issues were prevalent before the invasion of Russia into Ukraine, which caused global political havoc. Post-Russia-Ukraine war, the inflation concerns have worsened, which directly affects the availability of commodities like Ukrainian wheat and other essential pharmaceutical raw materials. Further, the growing number of sanctions by the western world on Russia, the third-largest exporter of oil in the world and largest exporter of wheat, has led to soaring prices of these commodities in the global markets.

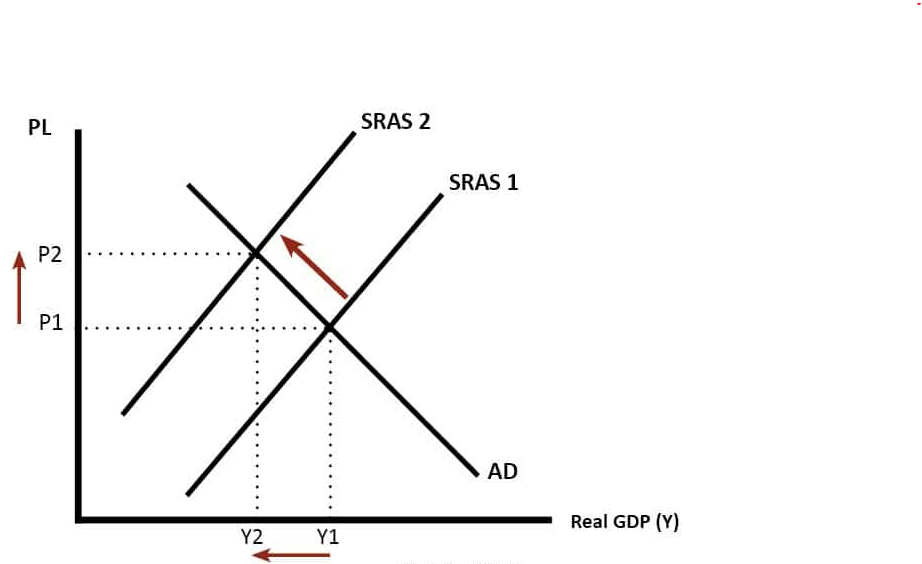

This will disrupt the global supply chain driving the prices even higher, and with Fed’s rate hike campaign, it can further cause a decline in GDP that could lead to a recession. The below-mentioned diagram indicates how higher oil prices increase the cost of firms causing short-run aggregate supply to shift towards the left. Also, the Aggregate Demand/Aggregate Supply diagram shows how higher oil prices impact the price level to move from P1 to P2 and lower the real GDP from Y1 to Y2.

How Do Stagflation Affect Investment Returns?

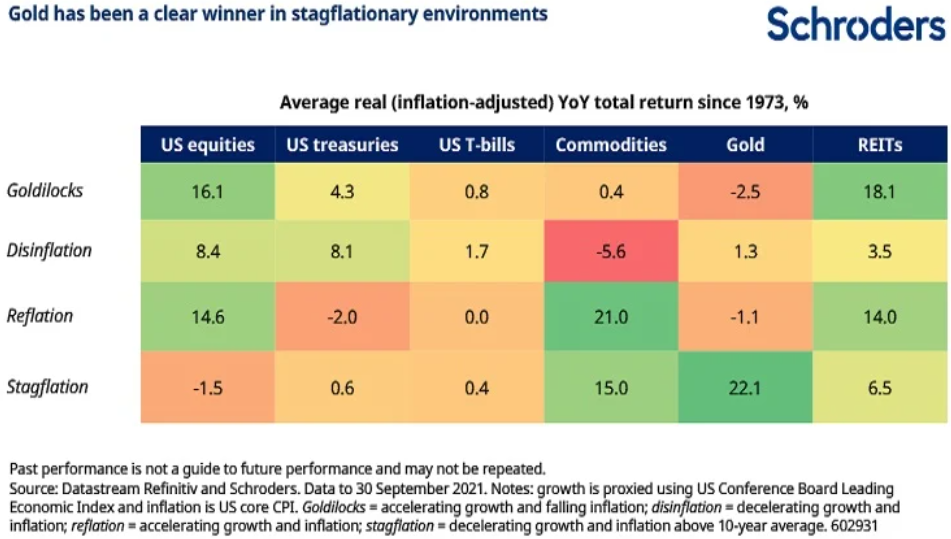

The first half of 2021 saw a strong rebound in economic growth alongside rising inflation which might be losing its momentum as fiscal and monetary stimulus fades away. The investment portfolio and asset allocation strategy also depend on the phases of the business cycle. It is based on the evolution of output and inflation that can be classified under four phases, namely: Goldilocks, Disinflation, Reflation, and Stagflation. During the post-COVID-19 recovery period, equities have soared globally, supported by high liquidity and government-led generous stimulus packages around the world. Although, a period of stagflation could favor more defensive assets such as gold which is often considered to be a safe-haven alternative in times of economic uncertainty.

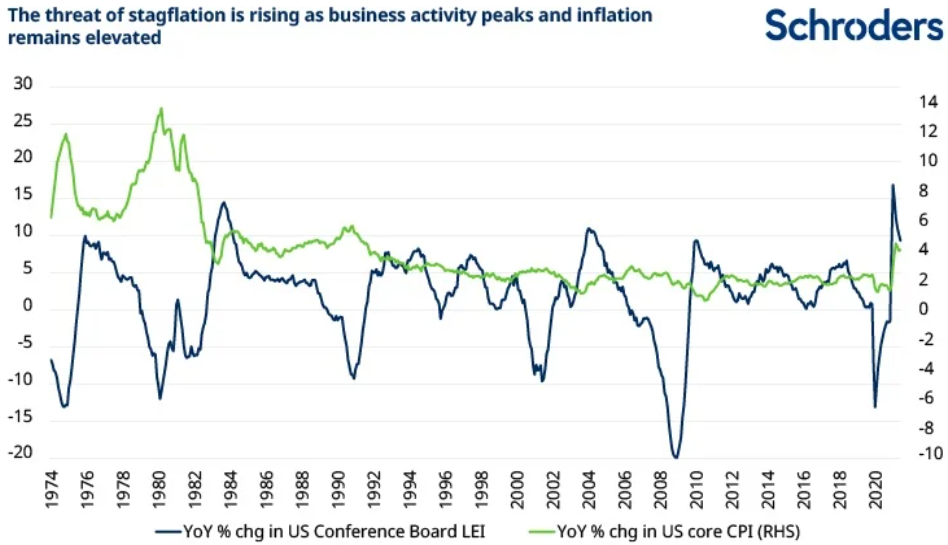

As markets are forward-looking, it can be challenging to evaluate asset class behavior during each phase of the business cycle which makes use of conventional measures of economic performance like GDP. It is a lagging indicator and may therefore inadequately capture pre-emptive asset flows. Therefore Schroders, an asset management firm, proxy growth using the US Conference Board Leading Economic Index (LEI), which is designed to signal turning points in economic data more effectively than GDP.

From the table mentioned below, we can see that Gold (22.1%) has been a clear outperformer in terms of returns during the stagflation period, followed by Commodities (15%) and Real Estate Investment Trust (6.5%). Although, Equities (-1.5%) have struggled to generate returns during stagflation as companies combat falling revenues and rising costs. During the stagflation period, commodities tend to perform well as they are the primary cause of rising prices that lead to inflation and benefits from the additional tailwind of growing economic demand.

Which Sectors To Invest In During Stagflation?

Commodities like precious metals, industrial metals, and other industrial & agricultural goods can help you weather a stagflation period. These are the essential commodities that come under the Energy, Metals, and Agricultural sector that causes inflation and increases the price of raw materials used in various industrial processes.

Additionally, due to the Russia-Ukraine war, the global supply chain has been disrupted, which has caused shortages in areas such as energy, semiconductors, agricultural goods, and raw material for pharmaceutical companies. Therefore, investors can adopt a barbell strategy and own cheap valuation stocks with high free cash flows and dividends.

Another approach could be investing in companies in upstream production that manufacture input goods for other industries and benefit from the soaring high prices during inflation.

Conclusion

The trifecta of subdued growth, high unemployment, and soaring inflation puts significant pressure on the economy leading to ‘Stagflation.’ It weighed heavily on the US through the 1970s, and there have been concerns that it may reemerge post COVID-19 economic recovery.

Economists are closely watching the trends in growth, unemployment, and inflation along with other potential catalysts that could trigger stagflation, including supply chain disruptions and central bank policies. Historically, gold, commodities, and REITs have been outperformers in terms of investment returns during the stagflation period. Therefore, investors should allocate a higher proportion of their capital towards these asset classes and less towards equity.

No comment yet, add your voice below!