While global economies have been on a roller coaster ride over the last two years, stock markets around the world have been booming and have reached all-time highs this year. 2021 appears to be the strongest year for IPOs and listings, with 2388 IPOs raising approximately US$453.3 billion. Worldwide activity has also increased as a result of the inorganic growth of firms in the aftermath of the epidemic and subsequent recovery.

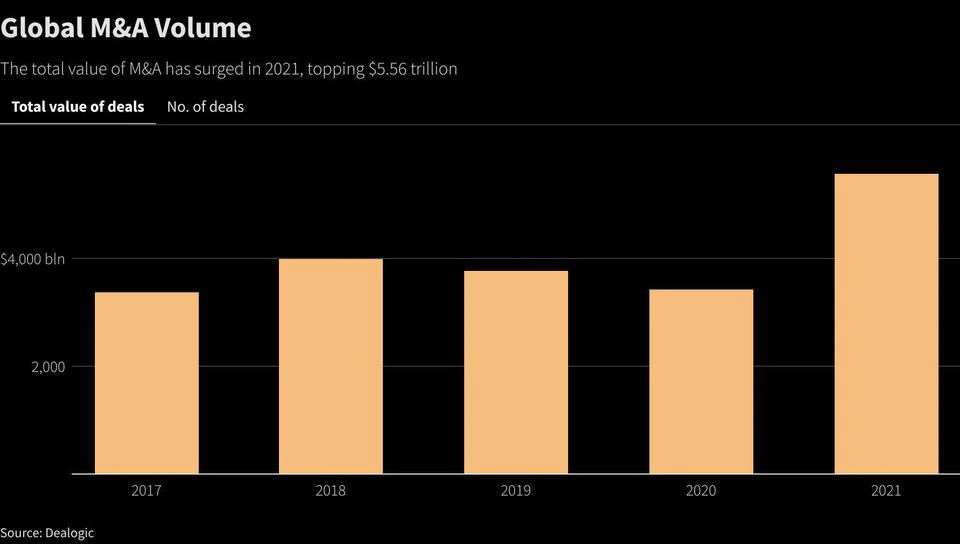

Global M&A value reached $5 trillion for the first time, with volumes climbing 63 percent to $5.63 trillion by mid-December, far beyond the pre-crisis high of $4.42 trillion in 2007.

Factors driving these records to break

A variety of factors have led to the recent increase in Mergers and Acquisitions. Internal factors influencing the volume of M&A deals include the company’s core competencies, strengths, and constraints, as well as the negotiating power of its buyers and suppliers. External factors such as the industrial structure, level of competition in the industry, and government-mandated regulations and policies are often considered as major catalysts for M&A activity.

Mergers and acquisitions of this type typically seek economies of scale, diversification, increased market share, increased synergy, cost reductions, or new niche offers. They can also be used to enter into a new market or to reduce surplus capacity and competition. Companies seek cost-cutting measures to increase value through mergers. Stock swaps can assist in overcoming the challenges of relatively high valuations. A record number of megadeals worth more than $5 billion were announced in the first half of 2021, with expanded scale or transformational benefits cited as the strategic justification for several of these.

Companies seeking the benefits of size and scale have announced a significant number of recent mergers. Large firms appear to have fared better than their smaller, less well-capitalized competitors due to their efficient operations and easier access to money. Firms rushed to raise funds through stock or bond offerings. Financial sponsors pounced on publicly traded companies as equity markets rose, allowing large organizations to utilize their stock as acquisition money.

There are still headwinds from inflationary pressures. However, robust corporate earnings and an overall bright economic outlook gave businesses the confidence to pursue large transactions.

Industries Affected the Most By M&A Deals

Technology, financials, and healthcare have accounted for the majority of the M&A market in the past. They will lead the way again in 2021, fuelled in part by pent-up demand from the previous year, when M&A activity fell to a three-year low due to the global financial effect of the COVID-19 pandemic. Technology continues to dominate, with a 133 percent increase in global M&A so far this year, hitting an all-time high of US$888.2 billion in announced mergers. The industry now accounts for 20% of the M&A market, with financials coming in second with 12% of the global M&A market. A surge in interest in medical suppliers, contract research organizations, and biotech companies resulted in a banner year for healthcare dealmaking.

Investment Banks Are the Biggest Beneficiaries

Breaking apart corporate empires and conglomerates is a lucrative business for investment banks. Following a year of lockdowns, global investment banks urged their dealmakers to meet with more customers in-person to clinch lucrative bids to merge or defend them from activist investors. Almost every investment banking product has been in high demand. This year, most investment banks are projected to collect more than $100 billion in fees.

Rise of SPACs as a Mode of Raising Money

In early 2021, SPACs proliferated, with a record 274 new ones listed in the first quarter. They raised more than $80 billion in the first half of 2021 (primarily between February and March), which is more than they raised in the entire year of 2020. This level of expansion naturally grabbed the attention of regulators, investors, and the media. In April, the SEC issued new financial reporting guidelines for SPACs, resulting in several restatements. The number of new SPACs being formed has now decreased. Poor post-acquisition returns may also be a factor in SPAC decline. However, given their popularity as a means of taking certain sorts of businesses public, such as highly valued, technology-oriented, imaginative, or disruptive businesses, they are unlikely to fade away anytime soon.

Future Outlook

The rush to close deals shows no signs of abating ahead of potential interest rate hikes. Borrowing costs, on the other hand, are widely projected to climb in the coming months, with the Federal Reserve of the United States signaling that interest rates would be raised next year to combat rising inflation. Nonetheless, M&A activity is expected to be robust as a result of a growing desire for improved in-house skills.

No comment yet, add your voice below!