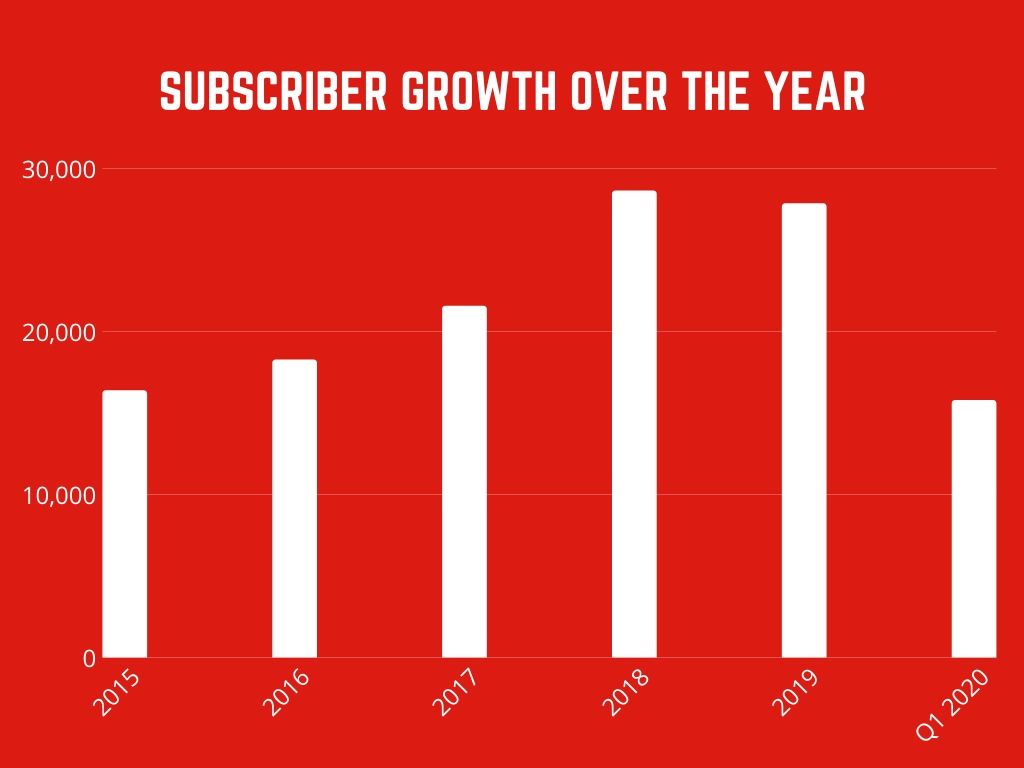

Giving back to back hit series and binding the whole country in an unprecedented time of pandemic inside their home like glue, Netflix has proven itself a means to kill boredom around the world. Due to this reason probably they recorded an impressive subscriber growth of 23% YoY, and global paid subscribers stood at 182.86 million.

| Region | Net Addition in this quarter (in millions) |

|---|---|

| UNCAN | 2.31 |

| EMEA | 6.96 |

| LATAM | 2.9 |

| APAC | 3.6 |

Netflix stocks have continued to perform well against market volatility. Uncertainty in the economy due to the counter cyclic nature of its growth metrics, this enormous increase in subscribers is contributed by March being an outlier as lockdown started in full swing in mid-march in most of the countries. On the content part, Netflix has assured its subscribers that they have a solid product pipeline till early 2021, which consists of more than 200 post-production projects, so there is no reason for the subscriber to worry about content even if the lockdown in countries is extended.

Orange Is the New Black in the market

It is evident that the current crisis has resulted in a boom for Netflix and the stock is up by 27.3% year to date, the major issue is with the new chunk of subscribers who are forced to stay at home and have subscribed getting nothing better than to watch television.

Taking a closer look at the subscribers, it tells us that Netflix has been consistent in adding subscribers. For this quarter, the sudden jump is due to home confinement; it would be interesting to see if these new subscribers will continue to stick with Netflix after this confinement period or if there will be a drop in the subscription in Q3 and Q4.

But what is good news for Netflix is human habits which are easy to form and tough to break, which tells that this habit may stick even after lockdown is lifted. We still expect that Q2 will be the biggest beneficiary of this growth as in Q2 the company harnesses the full benefit of home confinement.

Beauty and the Beast Valuation

With the share price $NFLX ($415.27) trading near the 52wk high and the current market cap of $182.6bn, for some, the stock seems expensive. But that undermines the ability of Netflix, which is on a long growth runway with the stickiness of its subscribers that tells how well Netflix is performing as compared to conventional TV subscription.

The concern of investors is, the stock has done so well amid the crisis, which has brought its valuation to a level that may prove difficult for H2. COVID19 has given a short term boost to the in the subscription but has also halted many of the projects of Netflix. Netflix will only continue them once the lockdown is lifted, which will be again financed with debt- given their negative cash flow, increasing the debt, which currently stands at $14.17bn.

Debt isn’t a bad thing, but rising debt, increasing competition, and sluggish growth in the North American market can turn out as a down signal for Netflix. The higher price seems like a bubble that cannot be justified with the result; hence it is being suggested by a few analysts to book profit and exit before it washes out the profits.

What is with the Disney +

Disney+ aka pandemic babysitter during this time of pandemic justified its launch by Disney last year. Media and parks being the biggest contributors of revenue have been heavily hit by the pandemic, and it is expected that it will plunge the revenue by 20%. Disney announced on April 08, 2020, that it had surpassed 50 million subscribers. For context, they were planning to hit 60-90 million by 2024; hence the growth in such a short term is phenomenal, but the challenge is to maintain profitability amid stiff competition.

Conclusion

It depends upon the risk appetite of an individual to take the risk; due to which the bubble sometimes seems interesting to some, while an opportunity for few to exit.

No comment yet, add your voice below!