Introduction

“Credit Suisse Is the Lehman 2.0?”

“Does “Too Big To Fail” Work in 2022?”

“What CDS?”

“Banks bad!”

With all the questions circulating in the financial coterie, we performed a deep dive and tried to gather insights about the current Credit Suisse situation.

Grab a cup of coffee. In layman’s language, this article discusses the too-big-to-fail phenomenon, the subprime crisis of 2008, Lehman Brothers bankruptcy, AIG’s bailout, Credit Default Swaps, and the current Credit Suisse situation. Ready?

Too Big To Fail

“Too big to fail,” as the name suggests, are institutions (mostly related to banking and finance) that are so large and interconnected that their failure would be disastrous to the entire economic system. Therefore, they are deemed supported by the government when they face a potential crisis. Empirically speaking, the government did bail out many institutions in the past. Except for a few!

Although the term was first popularized by US Congressman Stewart McKinney in 1984 (while discussing the Federal Deposit Insurance Corporation), it emerged as a prominent public term only following the global financial crisis of 2008.

Just after the financial crisis of 2008, former Fed chair Ben Bernanke (who oversaw the Fed’s response to the crisis; and was responsible for the bailouts. and the quantitive easing; and apparently, the one who recently won the Nobel Prize) defined TBTF as:

“A too-big-to-fail firm is one whose size, complexity, interconnectedness, and critical functions are such that, should the firm go unexpectedly into liquidation, the rest of the financial system and the economy would face severe adverse consequences. Governments provide support to too-big-to-fail firms in a crisis not out of favoritism or particular concern for the management, owners, or creditors of the firm but because they recognize that the consequences for the broader economy of allowing a disorderly failure greatly outweigh the costs of avoiding the failure in some way. Common means of avoiding failure include facilitating a merger, providing credit, or injecting government capital, all of which protect at least some creditors who otherwise would have suffered losses. If the crisis has a single lesson, it is that the too-big-to-fail problem must be solved.”

A Tale Of Two “Too-Big-To-Fail” Institutions

The housing bubble/subprime crisis of 2005-2010, where too many loans were given to people who couldn’t afford them, and too much money was thrown into the mortgage arena by investors who wanted to earn high-yield on their investments, had hazardous effects on a few of the largest investment banks, commercial banks, and insurance companies.

Some went bankrupt, some were acquired at throwaway prices, and some were bailed out by the government. Among them, the most notable institutions were Lehman Brothers, Bear Stearns, Merrill Lynch (Investment Banks), American International Group AIG (Insurance), Morgan Stanley, and Goldman Sachs (Commercial Banks). Let’s briefly understand what happened with Lehman Brothers and American International Group (AIG).

Lehman Brothers

| Primary Reason for Mishap | Subprime Lending |

| Too Big To Fail? | Too big, but failed; Government didn’t rescue |

During 2003 and 2004, while the US housing bubble was underway, a very confident (overconfident) Lehman went into an acquisition spree and acquired mortgage lenders that specialized in high-yield (thus high-risk) mortgages. The extent of risk was so high that most of these loans were disbursed without even proper documentation. These acquisitions yielded good returns till 2007, the time the housing bubble peaked.

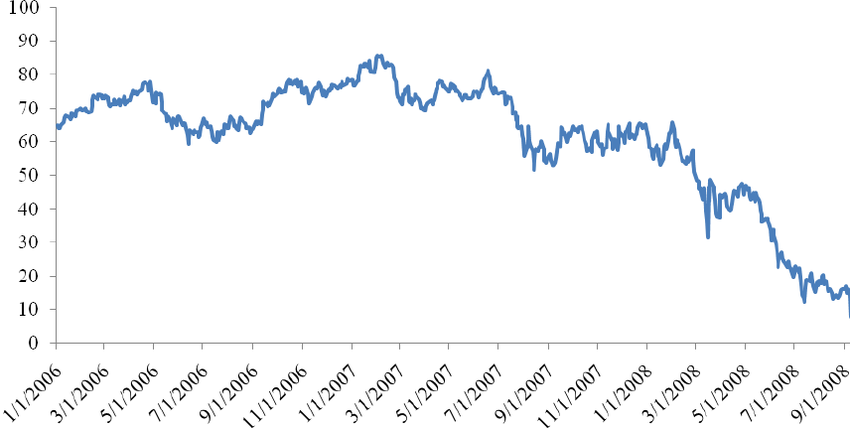

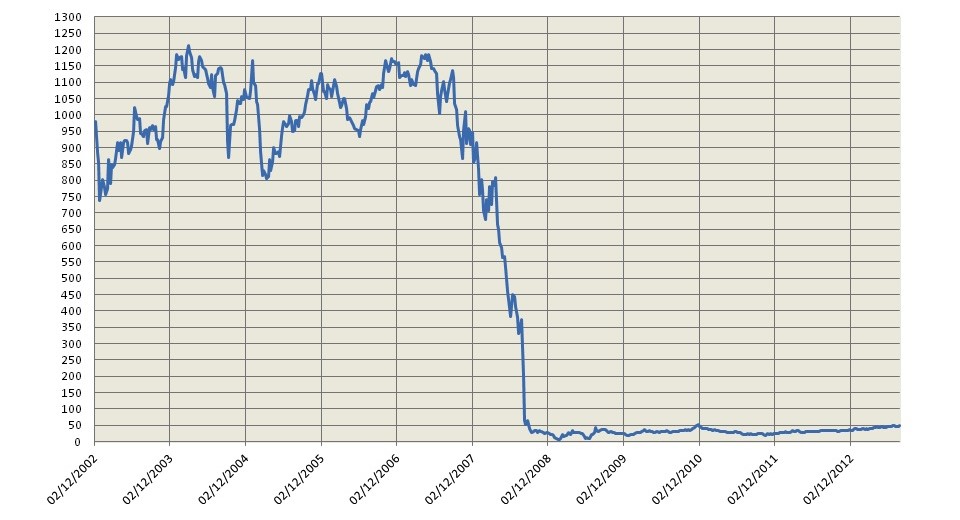

In 2007, Lehman Brothers wrote more mortgage-backed securities (e.g., housing loans) than any other institution in the world. By 4Q2007, it acquired a loan portfolio of $85 billion, a staggering four times its equity. Its leverage ratio touched an alarming high of 31. In February 2007, Lehman’s stock peaked at a record $86.18, with a market capitalization of ~$60 billion. Because of these high-yield investments, Lehman Brothers reported a record profit of $4.2 billion on ~$19 billion of revenue in 2007.

At the end of 1Q2007, the housing market’s cracks started becoming increasingly evident. As the bubble started busting, housing prices started falling rapidly. The price fall was so sharp that most of the houses’ value was now even lower than the loan payment remaining on them. As a result, people started defaulting on their loan payments (they were better off buying a new house than paying the remaining installments on their existing house). A full-blown housing crisis erupted in August 2007, and Lehman’s stock trajectory inverted. After years of increasing profits, it was only on June 7, 2008, that Lehman reported a second-quarter loss of a whopping $2.8 billion, after which its stock started plummeting sharply.

The firm’s Credit Default Swaps (CDS), which we will discuss shortly, started suffering a steep increase in their prices (an increase in CDS price is bad for the underlying institution); large investors started losing confidence in the company. The third quarter results (reported on 10 September 2008) were the final nail in the coffin, where they announced $3.9 billion in losses. Lehman was running out of time, with just $1 billion left in cash, and needed massive funds before the end of the week to stay solvent. On 13 September, Barclays and Bank of America made a last-ditch effort to take over Lehman Brothers but were ultimately unsuccessful.

On Monday, 15 September 2008, Lehman declared bankruptcy.

Lehman Brothers is a prime example of a “Too Big To Fail” institution that was not ultimately saved by the government. It is said that the government did not save Lehman because it did not have adequate collateral to support a loan, even under the Fed’s emergency lending power. Also, the US government could not save all of them and, for obvious reasons, decided to bail out an even bigger and interconnected American International Group (AIG).

AIG

| Primary Reason for Mishap | Credit Default Swaps (They insured toxic financial assets) |

| Too Big To Fail? | Too big; the Government rescued it. |

American International Group (AIG) was another big institution (insurance giant) that faced the wrath of the subprime crisis. It almost tasted a moribund situation until the Federal Reserve came to its rescue.

We discussed briefly how institutions like Lehman Brothers (and many more) disbursed highly risky loans, leading to the housing bubble, then to its burst, and ultimately to the subprime crisis of 2008.

Now, the problem was not limited to the institutions that were making subprime lending. There was a larger problem, where institutions like AIG were insuring these subprime loans! This type of insuring is done through a derivative instrument called “Credit Default Swaps,” or CDS.

Credit Default Swaps (CDS)

Imagine a large investor (such as a bank) buying some bonds issued by Apple. As per the conditions of the bond, the bank expects to receive regular coupon payments from Apple (that’s how a bond works). But the bank fears that there’s a chance that Apple might not be able to fulfill its payments (Suppose Apple goes bankrupt!). The probability is low, but not zero, and if it happens, the bank suffers. In this case, the bank might decide to buy a Credit Default Swap (CDS).

CDS is, basically, insurance on bonds. If Apple never goes bankrupt, the bank only loses the premium it paid for the CDS. But If Apple defaults and stops paying its bondholders, the bank gets money from the CDS seller.

AIG was one such institution that excessively sold these CDSs to investors of subprime loans (such as Lehman Brothers). It was easy money at that time since bond issuers almost never went bankrupt. So, many banks and insurance companies figured they could make big money by selling CDSs, just cashing in the premium, and never paying out anything.

So, what went wrong? With the housing prices crash, those mortgage-backed securities became worthless; and suddenly, that seemingly low-risk event of an actual bond default started becoming a daily affair. The banks and insurance companies selling CDSs were no longer enjoying “free” money; they now had to pay a lot more money than they ever earned selling these CDSs.

Coming back to AIG

Most institutions hedged their risk, i.e., they bought CDS protection on the one hand and sold CDS protection on the other (cashing in the spread, risk-free). In case of a bond default, the banks will need to pay the money to whom they sold CDS, but they’d also be getting money back from who they bought CDS.

Everyone except for AIG!

AIG was only on one side of these trades; they only sold CDS. AIG might have thought that CDSs are just an extension of the insurance business. But they’re not. In insurances like home, car, and life, you can expect steady, actuarially predictable trends. A fire in one home doesn’t increase the probability of fire in another; the death of one person doesn’t increase the probability of the death of another person.

But this is not the case with bonds. Once some bonds start defaulting, other bonds are more likely to default. The risk increases exponentially. And because AIG had just sold CDS, there was only an outflow!

At the onset of the subprime crisis, AIG wrote bond CDS of more than $440 billion. AIG didn’t have even half of the money to cover those. Their customers, those banks and hedge funds who bought CDSs from them, started getting nervous, and so did government regulators.

Too Big To Fail Interconnectedness

At the beginning of this article, we wrote that “Too big to fail” are institutions that are so large and interconnected that their failure would be disastrous to the entire economic system.

Let’s see what could have happened if AIG were not bailed out.

Banks across the world bought CDSs from AIG. If AIG cannot honor the payment as a counterparty, then all of those banks’ risk protection measures (to protect capital) will go for a toss. Overnight, the banks will have to look for replacement coverage at much higher rates (because the risks now are much worse than when AIG sold most of these CDS contracts).

In short, banks all over the world are instantly worth less money. The numbers seem huge, possibly in the hundreds of billions. To cover that rapid loss, banks will lend out less money. That means other banks can’t borrow to pay this new cost, and smaller banks might not have enough; they’ll collapse. That would further shrink the global pool of money. This will likely spur a whole new round of CDS payouts as all those collapsed banks issue bonds that someone, somewhere, sold CDS protection for. That new round of CDS payouts could cause another round of bank failures. A round of bank failures means a round of financial system collapse. Phew!

AIG Bailout

Ultimately, the U.S. government started AIG’s $182 billion bailout, ironically, the same week in which Lehman Brothers declared bankruptcy. Some say that the bailout of AIG, but not Lehman Brothers, was a politically inspired decision. Still, a larger opinion believes that AIG was more interconnected than Lehman, and its failure would have a domino effect on financial institutions worldwide.

Too Big To Fail Institutions – 2022

In 2021, the Financial Stability Board, a policy research and development entity, released a list of 32 banks worldwide that they considered “systemically important financial institutions”—financial organizations whose size and role meant that any failure could cause serious systemic problems.

| Agricultural Bank of China | China Construction Bank | Industrial and Commercial Bank of China Limited | Royal Bank of Scotland plc |

| Banco Bilbao Vizcaya Argentaria, S.A. | Citigroup | ING Group | Société Générale S.A. |

| Banco Santander, S.A. | Crédit Agricole Group | JPMorgan Chase | Standard Chartered plc |

| Bank of America | Credit Suisse Group AG | Mitsubishi UFJ Financial Group, Inc | State Street Corporation |

| Bank of China | Deutsche Bank AG | Mizuho Financial Group, Inc. | Sumitomo Mitsui Banking Corporation Group |

| Bank of New York Mellon | Goldman Sachs | Morgan Stanley | UBS Group AG |

| Barclays | Groupe BPCE | Nordea Bank Abp | UniCredit S.p.A. |

| BNP Paribas | HSBC Holdings plc | Royal Bank of Canada | Wells Fargo |

Current Scenario – Credit Suisse

Over the last few weeks, we have constantly been coming across headlines like “Credit Suisse: The Next Lehman?” “Credit Suisse: Crisis Suisse,” “Debit Suisse.”

Certainly, there’s a lot wrong with the bank (watch this interesting video by FT to know more), but is it so bad that it will ultimately end up like Lehman Brothers? Let’s see.

What caused the trigger? Credit Default Swaps!

We already discussed Credit Default Swaps in an earlier section. We know that the higher the risk of security defaulting, the higher its CDS cost.

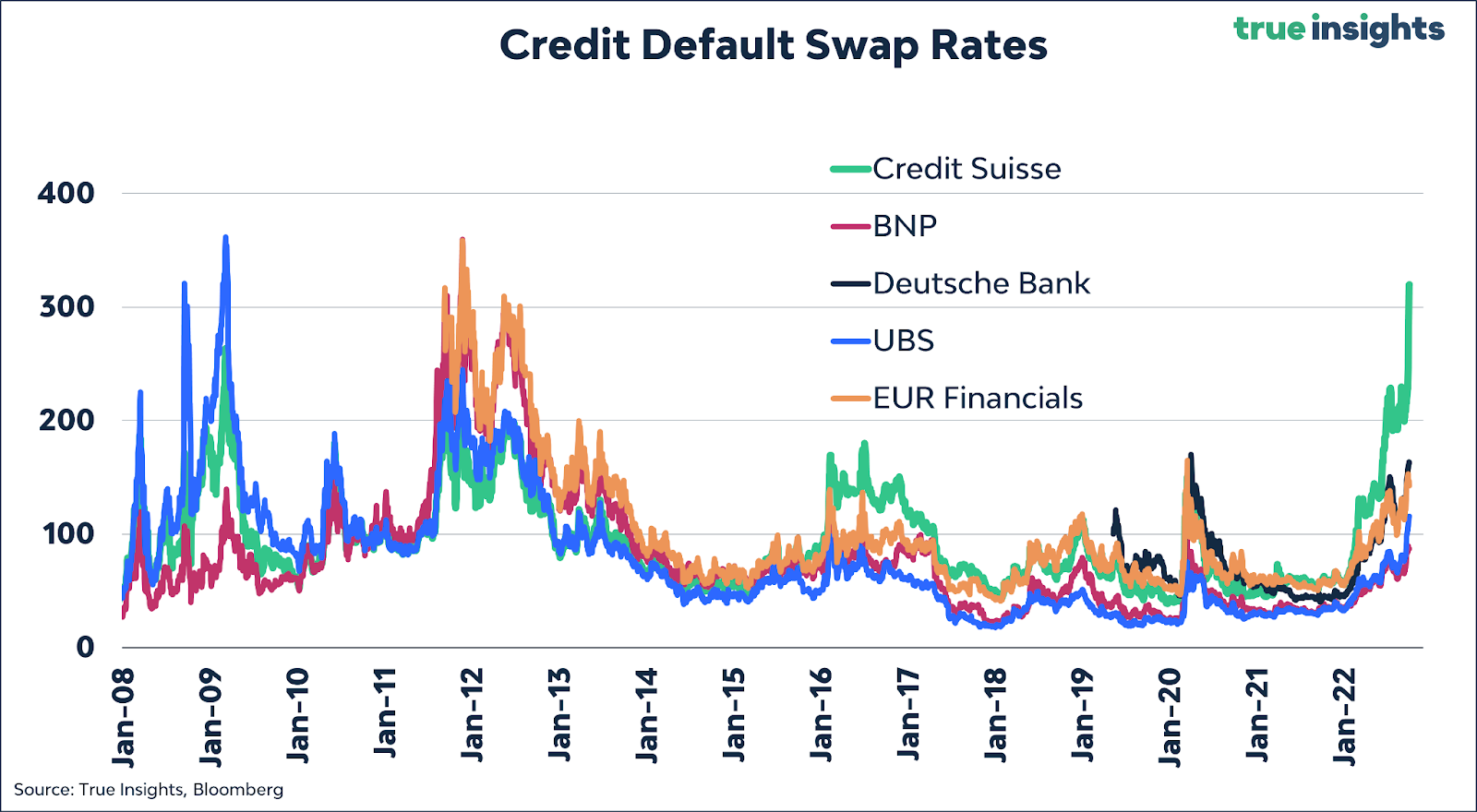

CDS cost is denoted as a percent of a securities face value. Credit Suisse’s stock has been declining steadily for the past few years, and on Monday, 3rd October 2022, Credit Suisse’s bond CDS spreads spiked to 14-year highs.

Credit Suisse’s CDS spread is above 300 bps, which is way beyond the 2008 market-implied default risk. Also, it is a clear outlier when compared to other similar banks.

But do you see an interesting observation? CDS spreads of ALL financials have risen considerably in 2022.

During the beginning of the housing crisis, Lehman Brothers was not initially on the verge of bankruptcy; they could have raised some money to keep them afloat. However, as sentiment got progressively worse about the high leverage of the bank, bankruptcy became a self-fulfilling prophecy.

Coming back to Credit Suisse, the actual default risk of the company (as implied by its balance sheet and capital structure) is elevated but not a cause for immediate concern. Market confidence is the key matter of concern for Credit Suisse in the near term. Confidence plays an integral role in credit markets.

The following is a default risk model for Credit Suisse on a Bloomberg Terminal. A default risk model is a more accurate representation of credit risk than just CDS spreads, evaluating the capital structure of the firm and not just its market-implied credit risk.

Credit Suisse has a 2.6% probability of default within the next year. Although, its industry neighbors in the United States have an average implied probability of default of ~0.05%. With 40% of CS’s debt being short-dated, its funding position is threatened by the rise in short-term rates. Going to the market and selling bonds to finance itself will be met with higher and higher rates during this period of faltering confidence.

| Credit Suisse | J.P Morgan | Goldman Sachs | |

| Default Probability | 2.6% | 0.05% | 0.08% |

| Market Cap. | $10.5 billion | $306.4 billion | $104.3 billion |

| ST + LT Debt | $269.1 billion | $2 trillion | $1.1 trillion |

| Return on Assets | -0.5% | 1.0% | 1.1% |

| Effective Net Income | -$1.14 billion | $8.4 billion | $2.8 billion |

The majority of Credit Suisse’s outstanding paper is short-dated—78% with a maturity of four years or less. Financing itself over the next few years while monetary policy remains tight is going to be a tall order for the heavily indebted Swiss bank as its reputation dwindles. But, Credit Suisse still has CHF44.2 billion of “going concern capital,” which is additional capital required by the Swiss regulators to absorb losses without triggering bankruptcy.

So, could Credit Suisse be the next victim of the tightest credit conditions we’ve seen in decades?

Not yet. However, this might be a 2023-2024 issue. Credit Suisse still has a lot of business divisions (such as Wealth Management, Banking, and Asset Management), which are doing decently. The major issue lies with its Investment Banking business. We believe that Credit Suisse is going through a bad time. But it’s not as bad as the media portrays it. Yet.

Conclusion

European banks are required to keep a Liquidity Coverage Ratio (LCR) at over 100%. This means they must always have enough High-Quality Liquid Assets (HQLA) to meet deposit outflows in a stressed situation. It’s worth noting that regulators view an LCR of anything above 110% as pretty healthy. Furthermore, the European Central Bank (ECB) can lend directly to banks at incredibly low rates for years.

Credit Suisse has an LCR of more than 190%, which is significantly higher than most of its peers. Probably, the key reason why Credit Suisse is getting punched right now is that it belongs to a very weak and cyclically exposed European banking sector that hasn’t been performing well. Further, Credit Suisse is one of the “Too Big To Fail” institutions, and not only the Swiss National Bank but even other central banks and big banks wouldn’t let it go down easily.

So, is it going to be Lehman Brothers 2.0?

Until now, Lehman Brothers is the only “TBTF” institution that went bankrupt, and for the obvious reasons that we have discussed. Further, this is not 2008; we now have stricter norms and regulations. Though everybody has been searching for the Lehman moment, it doesn’t look like this is it, yet.

Lehman was the cause, while Credit Suisse is a casualty. Rumors of insolvency run the risk of becoming a self-fulfilling prophecy, but still, it is less likely that CS will simply go down; a more likely situation is that it spins off its loss-making investment banking division, and a worst-case scenario would likely be that it gets acquired or merged with some other institution like UBS.

No comment yet, add your voice below!